The Stagflation Trap Is Closed

The Federal Reserve held the line. The system it was trying to stabilize did not.

The Fourth Turning Point — Thursday, April 30, 2026 | 16:36 EST

Jerome Powell put his glasses in his suit pocket and walked out of the room.

66 press conferences.

Eight years.

Done.

Brent surged 7.75 percent to $112.49 on the statement.

WTI broke $106

The 10-year Treasury climbed to ~4.4

Bond markets sold off globally.

Germany, France, Spain, Italy, the UK, and Australia all moved in the same direction.

National gasoline reached $4.23, up from $2.98 before the war began.

The market read the statement and reached its verdict in minutes.

Here is the verdict from this publication, first reached in October 2025 and confirmed today by the Federal Reserve itself.

The stagflation trap is closed.

The institution held.

The system did not.

The Statement

The Federal Open Market Committee held rates at 3.50–3.75 percent.

Third consecutive hold.

Expected.

The signal was not the decision.

The signal was the language.

Two sentences in the statement carried the entire message:

Developments in the Middle East are contributing to a high level of uncertainty about the economic outlook.

The Committee is attentive to the risks to both sides of its dual mandate.

Both sides of the dual mandate.

In 113 years of Federal Reserve history, that phrase appears when the institution faces simultaneous threats to employment and price stability.

That condition has a name.

Stagflation.

The Federal Reserve cannot say the word from the podium.

Those two sentences say it anyway.

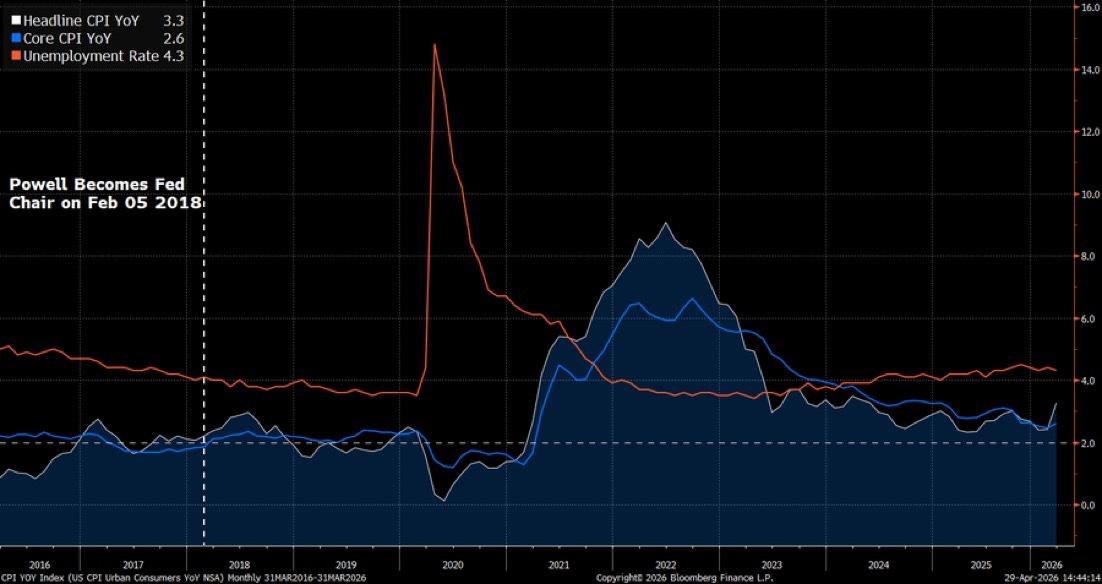

Powell named the drivers directly at the press conference.

PCE inflation: 3.5 percent over the twelve months ending in March, boosted by the surge in global oil prices following the Middle East conflict.

Core PCE: 3.2 percent, reflecting the effects of tariffs on goods prices.

Two inflation drivers.

The war.

The tariffs.

Both policy choices.

Neither addressable by the federal funds rate

The Dissents

Four dissents.

The most in 34 years.

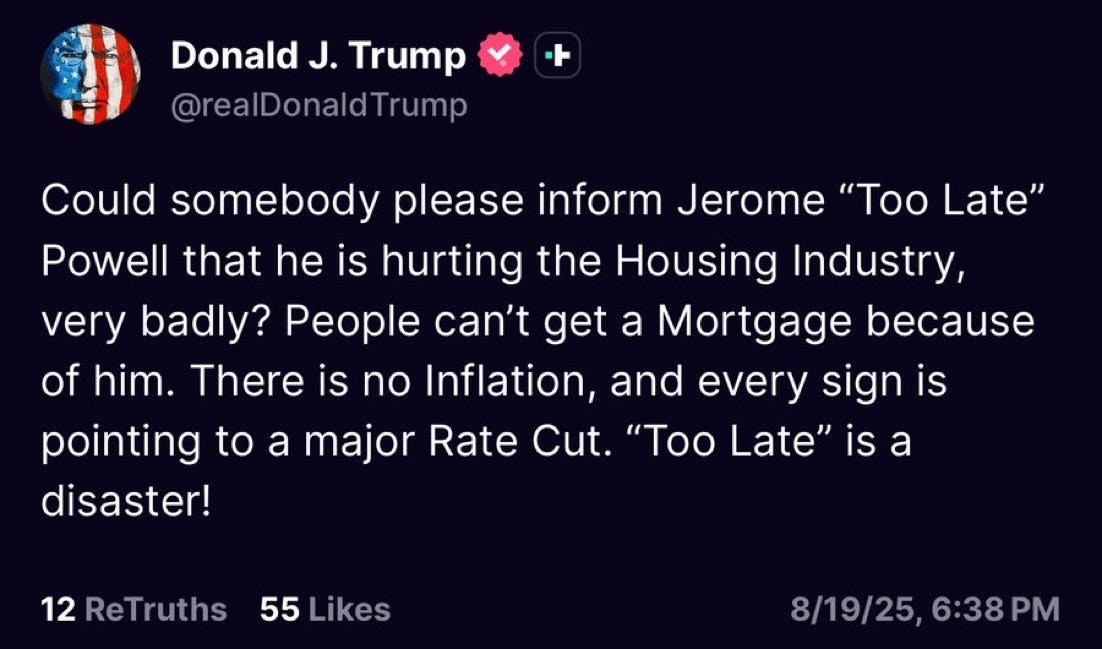

Stephen Miran, Trump’s own board appointee, voted to cut rates.

He has voted to cut at every meeting since September.

He voted to cut yesterday with Brent crude above $110, the OECD projecting 4.2 percent full-year US inflation, and the Strait of Hormuz closed for the first time in recorded history.

That is the policy outcome the administration wants, expressed as a dissent in the public record.

Three others dissented in the opposite direction.

Hammack.

Kashkari.

Logan.

They held the rate but refused any easing bias in the statement language.

They looked at the inflation data and concluded that even the subtle forward guidance embedded in the word adjustments was too generous to the idea of future cuts.

Powell held the institution between those positions for one final meeting.

Eight votes held the center.

Four pulled in opposite directions.

The committee that produced yesterday’s statement is not unified.

It is being pulled apart by the same political and economic forces this publication has been documenting for months.

The Incentive Structure

When a system behaves against its stated principles, identify who benefits.

The administration benefits from cheap borrowing.

Rate cuts reduce the cost of financing $36 trillion in federal debt.

The political cost of servicing that debt falls before November.

The inflation cost of cutting falls on consumers after November.

This is an incentive structure producing predictable behavior.

Concentrated corporations benefit from supply shocks.

In oligopoly markets, cost increases become pricing opportunities.

The top ten companies in the S&P 500 now represent roughly one-third of the entire index, the highest concentration in modern market history.

When the fertilizer shock reduced supply, every link in the food chain raised prices and expanded margins.

Few will lower them when the shock eases.

Politicians benefit from delayed pain.

Structural reform produces near-term costs and long-term benefits.

Electoral incentives run in the opposite direction.

The people who built this trap did not miscalculate.

They made a rational choice inside a political incentive structure that rewards the delay of consequences.

The cost falls on the households doing their own arithmetic at the kitchen table every month.

How the Trap Works

Stagflation eliminates the central bank’s ability to help.

The reason is mechanical.

The Federal Reserve has two primary tools.

Each addresses the opposite problem.

Cut rates and inflation accelerates.

Raise rates and the labor market fractures.

Hold rates and the energy-driven inflation the Fed cannot control continues printing in the monthly data.

There is no clean path through this configuration.

The playbook does not exist.

The current configuration is a hybrid.

An energy-driven supply shock layered onto the late stage of a debt cycle.

Both forces are present.

Both were acknowledged yesterday in the FOMC statement and from the press conference podium.

The data confirms it.

PCE inflation: 3.5 percent.

OECD projection for 2026: 4.2 percent, nearly double the Fed’s own estimate.

University of Michigan consumer sentiment: 47.6, the lowest in 74 years.

Gallup economic confidence: −38, below the April 2020 pandemic low.

A dollar in 2021 now buys eighty-two cents of goods.

This thesis has clear falsification conditions.

If oil returns below $80 and inflation expectations move back toward the Federal Reserve’s 2 percent target range, the stagflation thesis weakens materially.

Every falsification condition published here in January 2026 remains unmet.

The Debt Constraint

US government debt now exceeds 120 percent of GDP.

The IMF projects 140 percent by 2031.

Household debt stands at $18.8 trillion.

Private credit markets carry significant rate sensitivity across the system.

The constraint is mechanical.

Raise rates aggressively and debt servicing costs accelerate across every layer of the economy simultaneously.

The system is too leveraged to absorb Volcker-style tightening without triggering the credit stress that converts stagflation into deflationary collapse.

Cut rates and inflation expectations become unanchored.

The University of Michigan one-year inflation survey already sits at 4.8 percent.

The divide inside the Federal Reserve reflects two rational responses to the same trap.

Stephen Miran voted to cut rates.

Hammack, Kashkari, and Logan refused the easing language.

Each faction is reacting to a different side of the constraint.

One side sees the debt sensitivity of the system.

The other sees the inflation risk of easing policy too early.

Both are responding rationally to two halves of the same trap.

Powell held the center for one final meeting.

The Energy Transmission Mechanism

The Strait of Hormuz carries roughly 20 percent of global seaborne oil.

Closed since February 28.

The International Energy Agency calls it the largest energy supply disruption in recorded history.

Energy does not enter inflation directly.

It moves through the production system first.

Transport.

Fertilizer.

Plastics.

Food production.

Only after those costs move does the shock appear in headline CPI.

The fertilizer channel is already breaking.

Gulf urea production has fallen 60 percent since the war began.

The Middle East supplies roughly 45 percent of global urea trade.

Food inflation is accelerating as a result.

Powell said it directly from the podium yesterday.

Higher energy prices will push up overall inflation in the near term. Beyond that, the scope and duration of potential effects remain unclear, as does the future course of the conflict itself.

The constraint is simple.

Interest rates do not produce oil.

They do not reopen straits.

They do not restore fertilizer supply chains.

The primary inflation driver in this environment is geopolitical.

The primary tool of monetary policy addresses the wrong variable.

The Global Picture

Bond markets in Germany, France, Spain, Italy, the United Kingdom, and Australia all sold off after the statement.

The signal transmitted globally and immediately.

The reason is structural.

The US dollar remains the world’s reserve currency, and US monetary policy sets the baseline cost of capital for dollar-denominated debt across the global financial system.

When the Federal Reserve acknowledges a stagflationary configuration without a clear resolution timeline, global dollar funding markets reprice at once.

Other central banks are already recognizing the same risk.

The Bank of Korea flagged stagflation concerns.

The South African Reserve Bank named it explicitly in its April monetary policy review.

S&P Global’s flash PMI data confirmed the pattern across major advanced economies:

Output slowing.

Prices accelerating.

Across the United States, the United Kingdom, the eurozone, and Japan.

This is a global supply shock moving through financial systems that a decade of near-zero interest rates left maximally vulnerable to disruption.

The Federal Reserve acknowledged the signal yesterday.

Every central bank in the world received it at the same moment.

Jerome Powell

When asked how he wants to be remembered, Powell answered simply:

“I’m just going to say that’s for someone else to say.”

So here it is.

Jerome Powell held the Federal Reserve’s institutional independence against the most sustained and direct assault in its 113-year history.

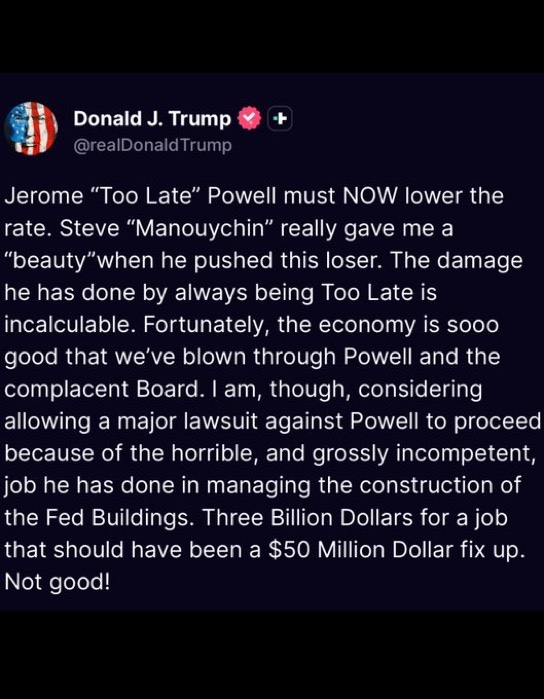

He held it through public insults from the president who appointed him.

Through a criminal investigation intended to pressure him into compliance.

Through an attempted removal of a fellow Fed governor.

Through Stephen Miran’s repeated votes to cut rates at every meeting since September.

He held it one final time yesterday, assembling eight votes against four pulling in opposite directions.

He never cut rates for political reasons.

He never raised them for political reasons.

From the podium yesterday, Powell said it directly:

“These legal actions by the administration are unprecedented in our 113-year history. I worry that these attacks are battering the institution and putting at risk the thing that really matters to the public.”

He named it.

He placed it in the official transcript.

The record now stands.

Arthur Burns chose accommodation.

Powell chose the institution.

Burns became a cautionary lesson in central-bank history.

Powell will become a case study in institutional character under political pressure.

History will record the difference correctly, even if the present moment does not.

Kevin Warsh assumes the chair on June 16.

He inherits:

a Federal Reserve committee split 8–4

an OECD inflation projection of 4.2 percent

a Supreme Court case that may determine whether presidents can remove Fed governors at will

a Justice Department investigation dropped conditionally, with the explicit option to reopen it

Whether Warsh defends the institution the way Powell did is now the central open question in American economic policy.

The Final Verdict

The trap did not appear by accident.

It was built.

Built by cheap money that created the fragility.

Built by tariffs that embedded inflation before the war arrived.

Built by a war started without authorization and without an exit strategy.

Built by the systematic removal of the institutional guardrails designed to prevent exactly this configuration.

Powell named it yesterday.

He called it unprecedented.

He called it a battering of the institution.

He placed the warning in the official transcript of his final press conference.

The record now stands.

The market registered the moment immediately.

The 10-year Treasury at ~4.4.

National gasoline at $4.23.

On the same afternoon Powell walked out of the room, Kevin Warsh’s nomination advanced 13–11 on a party-line vote.

The people who build traps rarely dismantle them.

That work falls to the next generation, after the damage is visible and the cost of avoiding it has already been paid by the people who could least afford it.

That generation is here.

The record stays public.

The positions remain disclosed.

Kevin Warsh sits down on June 16.

The work continues.

See you soon.

I, unluckily, understood this at first reading. Powell achieved several good things under Biden and the Trump, only to be dismissed by that narcissist. Now, whom is that Blob going to blame for the next catastrophe?

Really impressive analysis. Disclaimer, I share most of your frameworks, so it's a confirmation bias ( i learned about Howe thought , thanks for that).

Mainly Logo, and just enough pathos so this is not boring. Hardly believe you are only 22 !