The Reckoning Is Already Here

The Signal was always here. Now everyone can see it.

The Fourth Turning Point — Tuesday, April 21, 2026

A note before we begin

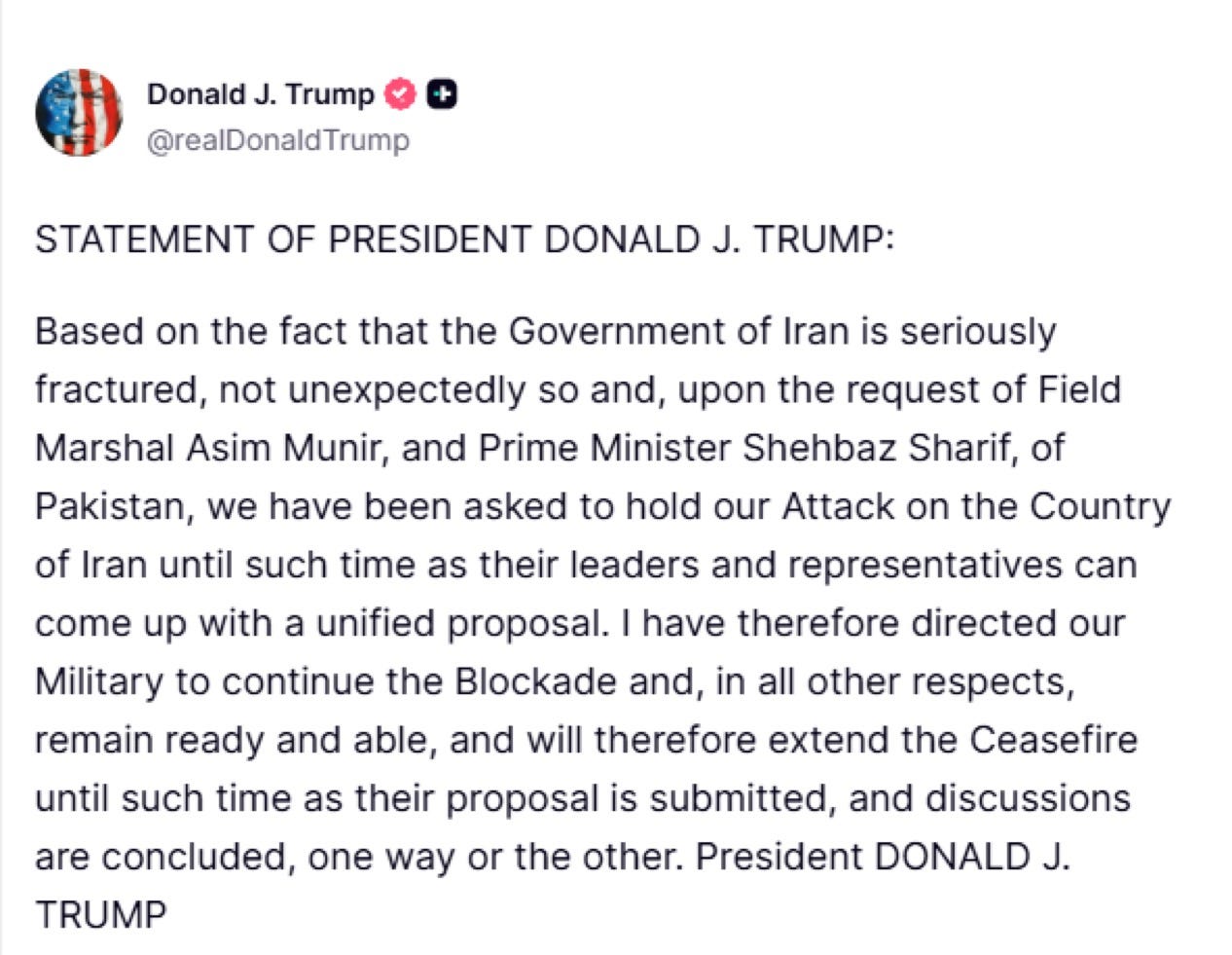

Trump just extended the ceasefire by Truth Social post, citing Iranian internal fracture and a request from Pakistan’s Field Marshal Munir. Iran immediately rejected the extension.

State TV says Iran does not recognize it and will act according to its national interests.

The IRGC’s Khatam al-Anbiya command says forces are at 100 percent readiness and any attack triggers immediate strikes on pre-designated targets. An advisor to Ghalibaf called the extension a ploy to buy time for a surprise strike and said the time for Iran to take the initiative has come.

Iran also displayed a Khorramshahr ballistic missile in a nighttime parade in Tehran with Qatar’s RasGas facility printed on it as a labeled target.

Four US KC-135R Stratotankers are currently flying over the Middle East. A Royal Air Force Voyager is over the Eastern Mediterranean.

The ceasefire has been extended by one side. The other side has rejected it and is publicly discussing striking first.

This publication went quiet for eight days because the foundation needed work.

The about page is rebuilt.

The schedule is fixed.

The architecture is designed for the long run.

Noise is easy.

Institutions are harder.

I wanted to come back stronger than I left, not just louder.

What follows is the live picture.

The strait.

The markets.

The electoral pressure.

The deeper work comes Wednesday and Saturday.

The framework synthesis.

The system analysis.

The historical argument.

The record is public.

The positions are disclosed.

Every call here was made before the outcome was known.

Now let’s get into it.

The Chokepoint of the World

Three realities now define the crisis in the Strait of Hormuz: a military standoff, collapsed negotiations, and the largest energy disruption in modern history.

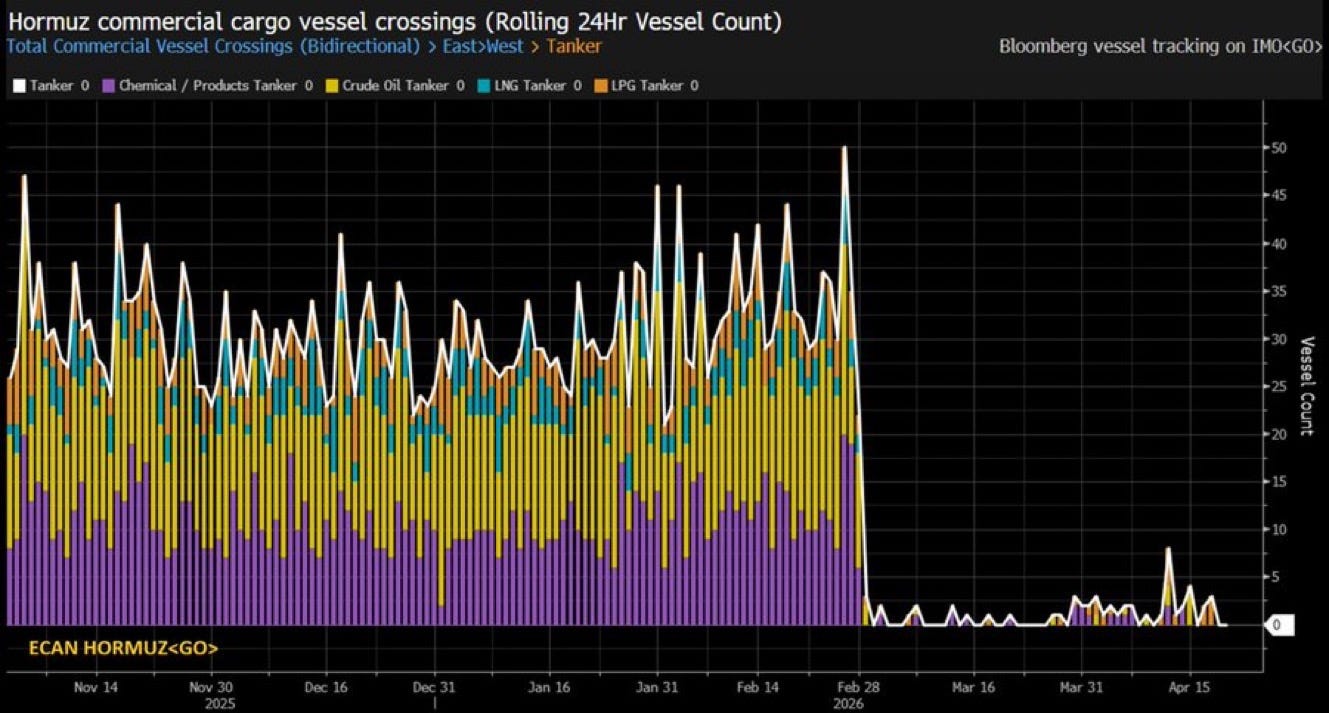

The Strait of Hormuz is functionally closed.

Near zero tankers transiting today.

First time in recorded history.

Not the largest disruption since last year.

Not the largest since 2008.

The largest disruption in modern energy markets.

Roughly one fifth of the world’s seaborne oil passes through the Strait of Hormuz, making it the single most critical energy chokepoint in the global economy.

The International Energy Agency calls it the greatest global energy security challenge in history.

Those are the words of the institution responsible for global energy security.

The Signal Before the War

In January 2026, three weeks before the first bomb fell, I published The Trump-Iran Moment.

The argument was not complicated.

When EA-18G Growlers deploy alongside missile defense repositioning alongside forward tanker movements, you are not watching deterrence signaling.

You are watching the final checklist before an offensive operation.

The decision window had already narrowed to three men.

Every other actor was downstream of their choices.

I wrote then that Iran does not need to close the strait to cause catastrophic damage.

It only needs to make insurers hesitate.

War risk premiums have since surged roughly 100 times pre-crisis rates.

For a single VLCC that is now a $10 to $14 million premium per voyage.

The waterway did not need to close for the damage to become historic.

It closed anyway.

Three weeks later, my warning became reality.

The Opening Strike

The war began February 28 during active nuclear negotiations.

Four days before talks were scheduled to resume.

While the Omani foreign minister was publicly saying peace was within reach.

His assessment after the strikes was blunt:

This was an attempt to reorder the Middle East in Israel’s favour.

The opening day strike destroyed a girls elementary school in Minab, killing at least 175 people, mostly children.

Multiple independent investigations later concluded the strike used outdated targeting data.

UN human rights experts characterized it as a potential war crime.

The administration is still investigating.

The children are still buried.

Negotiations Break Down

This morning Iran’s foreign ministry says it has no plans for the next round of negotiations.

Parliament Speaker Ghalibaf posted on X that Iran does not negotiate under the shadow of threat and that Tehran has prepared new battlefield options.

IRGC Commander Ahmad Vahidi, currently the only Iranian official with direct access to Supreme Leader Mojtaba Khamenei according to Israeli media, is reported to have the upper hand in the regime’s internal debate.

Trump told PBS yesterday that if the ceasefire expires without a deal, “lots of bombs start going off.”

Asked whether Iran will show up in Islamabad, he said:

“I don’t know.”

That is the state of play on the morning the original ceasefire expires.

The Strategic Reality of the War

From Briefing 1 through Briefing 11, the core thesis here has not moved once.

The original objectives of this conflict were unachievable from the start.

Regime change and the elimination of the IRGC were never realistic outcomes of an air campaign against a nation of 90 million people with 47 years of preparation for exactly this scenario.

I wrote that before the war began.

The current negotiating dynamic is its confirmation.

Power Consolidates Inside Iran

The IRGC has used this conflict to consolidate domestic power rather than lose it.

US intelligence assessments describe the IRGC as exerting greater control than before the first strike.

Vahidi is considered a radical even within Iran’s hardline elite.

His elevation is not moderation under pressure.

It is the exact opposite.

One Israeli analyst described it this week as “Islamic Republic 3.0.”

That framing is accurate.

Leadership Vacuum

Mojtaba Khamenei was appointed Supreme Leader on March 8.

He has not made a single public appearance in nearly six weeks.

Reuters sources describe injuries from the opening strikes.

He participates in governance only via audio conference.

An AI-generated video claiming to show him at a war command center was fact-checked as fabricated within days.

The legitimacy vacuum at the top of the Iranian system is real.

And it is being filled almost entirely by the IRGC.

That is the new structure of Iranian power.

Every negotiation now runs through it.

Terms No Iranian Government Can Accept

The 15-point plan delivered via Pakistan on March 25 demanded:

• dismantlement of Natanz, Isfahan, and Fordow

• an end to domestic uranium enrichment

• full IAEA monitoring

• missile program limits

• termination of proxy support

For context, the JCPOA agreement that Trump withdrew from in 2018 permitted enrichment up to 3.67 percent and required no facility dismantlement.

Iran is now being asked to accept terms harsher than the deal it rejected before the war, after absorbing the war.

Tehran called the plan excessive, unrealistic, and unreasonable.

The Islamabad talks ran 21 hours across three rounds.

No deal.

No memorandum.

The highest-level US-Iran meeting since 1979 produced nothing binding.

Iran rejected the second round before it began.

Strategic Contradiction

Iran Deal — Obama Administration

• Strait of Hormuz open to global shipping

• Iran limits uranium enrichment

• Iran commits to no nuclear weapons

• Iran allows international inspectors

• Inspectors confirm Iranian compliance

Iran Ceasefire — Trump Administration

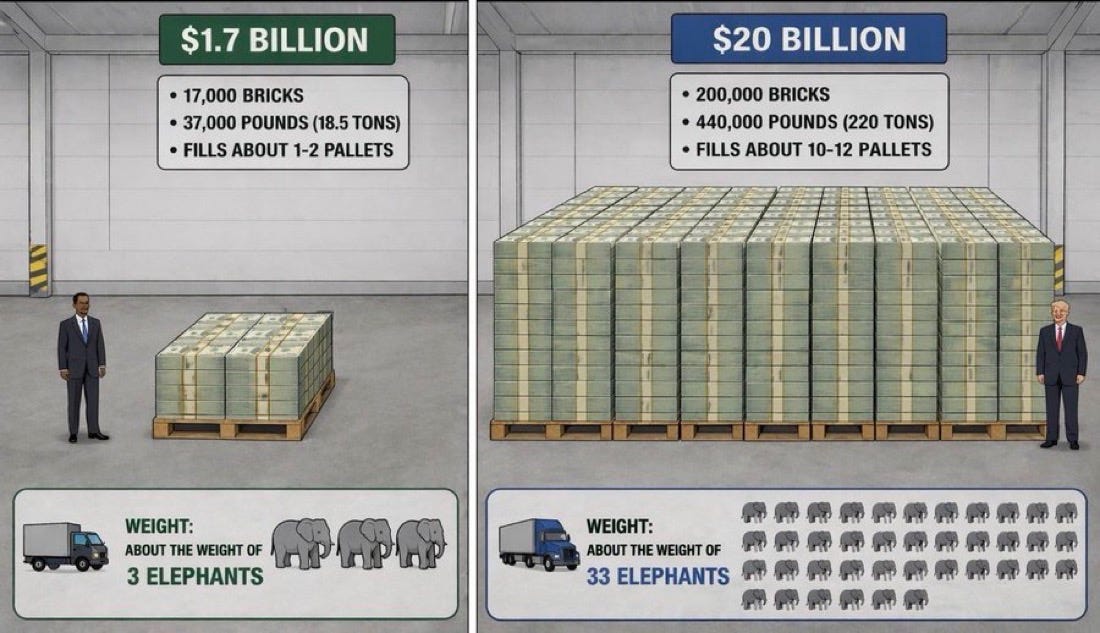

• Strait of Hormuz closed — reopening fees reportedly near $2 million per ship

• No commitment limiting uranium enrichment

• No commitment abandoning nuclear weapons

• No commitment allowing international inspectors

In other words:

A deal politically toxic for Iran has somehow been replaced by a deal strategically worse for the United States.

The Confession

On April 16-17 Trump told reporters Iran had agreed “very powerfully” that it would not develop nuclear weapons.

He also said he was no longer concerned about enriched uranium buried underground.

Iran immediately denied every characterization.

The war was justified publicly as preventing Iranian nuclear capability.

The president now says he is unconcerned about the uranium that still exists.

The people who died between those two statements died inside that gap.

Call it what it is.

A confession that the original objective was either never achievable or never the real objective.

The Blockade Within the Blockade

Former British Royal Navy commander Tom Sharpe described the current US posture as “the blockade within the blockade.”

Washington is attempting to inflict enough economic pain to force Iran back to negotiations.

Sharpe’s assessment:

Iran has shown it is willing to absorb extraordinary damage to ensure regime survival.

And the current pain level is nowhere near the threshold required for capitulation.

He is right.

The IRGC has been preparing for this confrontation since 1979.

They are not surprised by the pressure.

They trained for it.

The Supply Math

The supply math does not care about diplomatic timelines.

Even if a ceasefire were signed today:

Floating tankers require 30–40 days to unload.

VLCCs rerouted to the United States require three months or more to return.

Onshore Middle Eastern storage must drain roughly 200 million barrels first.

Projected cumulative supply disruption:

• 1.2 billion barrels by end of April

• 1.59 billion by end of May

• 1.98 billion by end of June

Four times larger than any supply outage in recorded history.

Kuwait declared force majeure on oil shipments this morning.

The IEA estimates Europe could run out of jet fuel within six weeks.

By late July, US commercial crude storage could fall below 400 million barrels, near operational minimum.

At that point the administration faces a binary choice:

Ban crude exports.

Or watch US refineries begin shutting down.

Neither option is compatible with governing through a midterm election.

Iran’s Long Game

The Iranian Parliament is drafting legislation to:

• ban Israeli-linked vessels from the strait

• require hostile states to obtain Iranian approval for transit

• block countries that damaged Iran until reparations are paid

This is not negotiation.

It is an attempt to codify permanent control of the world’s most critical energy chokepoint into domestic law.

Iran intends to own this lever permanently.

The Domestic Constraint

In The Trump-Iran Moment, I wrote that you cannot bomb your way out of an affordability crisis.

National gasoline has already peaked near $4.14 per gallon.

The Strategic Petroleum Reserve fell 4.2 million barrels last week, the largest draw since the Russian invasion of Ukraine.

The SPR was built for exactly this scenario.

And it is draining rapidly.

The Political Clock

The hard ceiling on this conflict was always the midterm calendar.

A president with 37 percent approval cannot sustain $4 gasoline heading into November.

That constraint was true in January.

It is more true now.

Everything in this conflict is negotiable.

That calendar is not.

Trump knows it.

Iran knows it.

And according to analysts cited in The Hill, Tehran believes it can simply wait him out.

Where The System Stands Now

The strait is closed.

The clock is running.

And the people with the most leverage over the outcome are the ones with the least incentive to hurry.

The strait is the geopolitical shock.

The market is where that shock eventually lands.

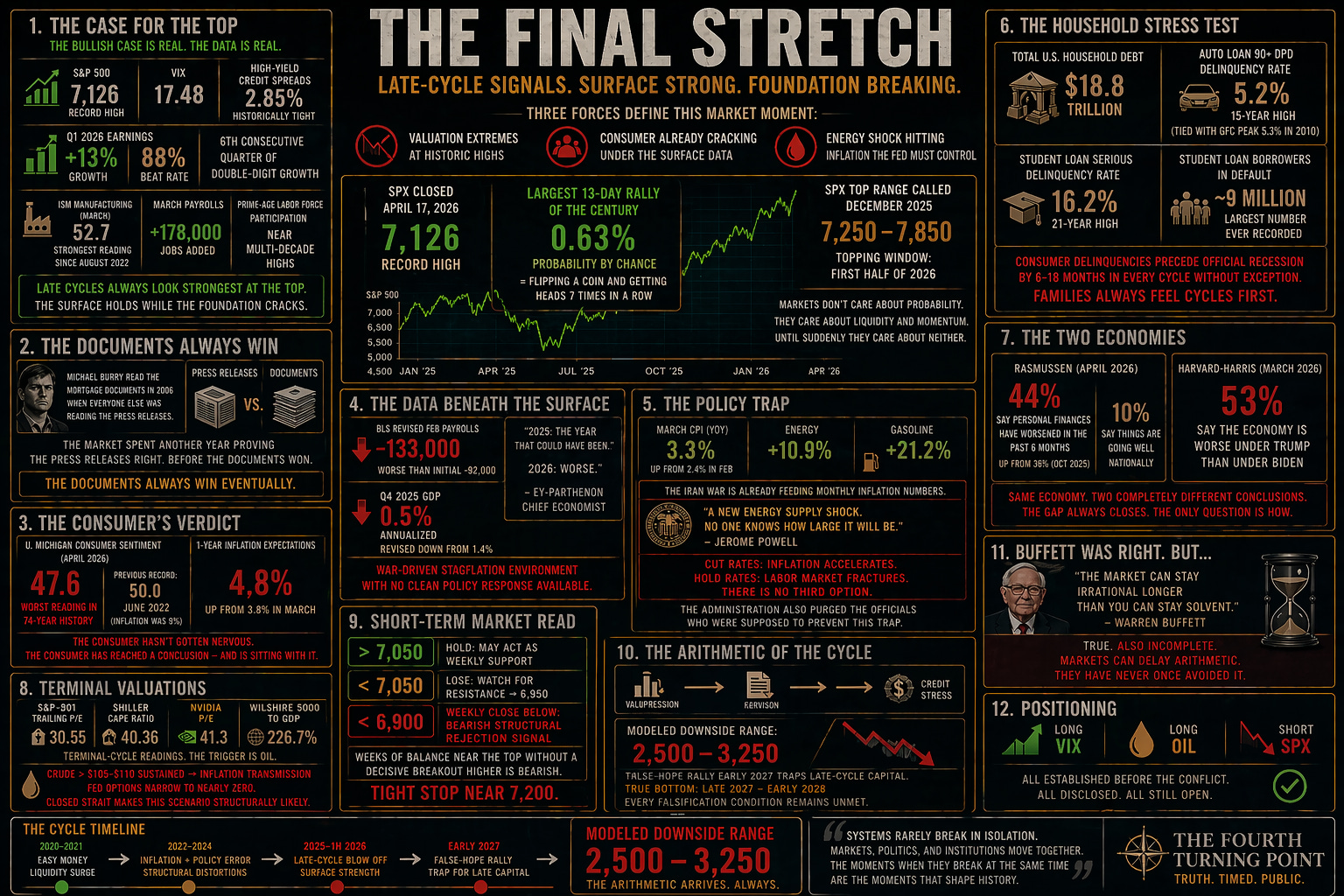

The Final Stretch

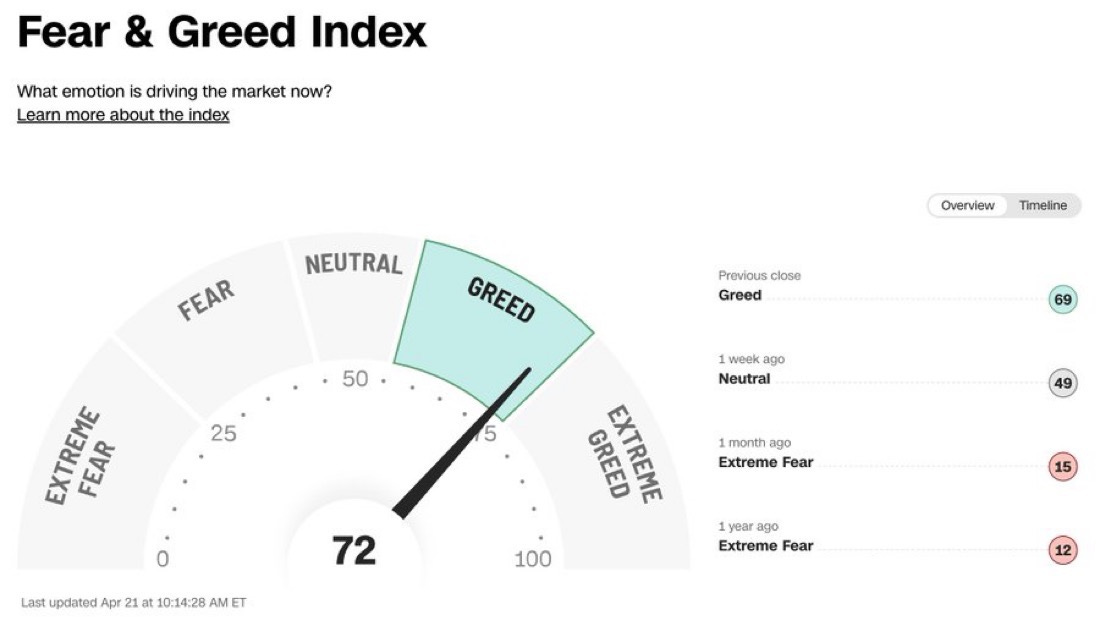

Three forces now define this market moment: valuation extremes at historic highs, a consumer already cracking underneath the surface data, and an energy shock moving directly into the inflation numbers the Federal Reserve is supposed to control.

In December 2025 I published The Final Stretch of This Market Cycle and called the SPX top range at 7,250 to 7,850 with the topping window in the first half of 2026.

The index closed at 7,126 on April 17, a record high.

The S&P 500 just completed the largest 13-day rally of the century.

The probability of that occurring by chance is 0.63 percent.

Roughly the same odds as flipping a coin and getting heads seven times in a row.

Markets do not care about probability.

They care about liquidity and momentum.

Until suddenly they care about neither.

The Case for the Top

The bullish case deserves a full hearing.

Anyone who skips the counterargument is not doing analysis.

They are writing a press release for their own position.

The SPX at a record high.

VIX at 17.48.

High-yield credit spreads at 2.85 percent, historically tight, with no credit stress signal anywhere in the data.

Q1 2026 earnings running +13 percent with an 88 percent beat rate, the sixth consecutive quarter of double-digit growth.

ISM Manufacturing at 52.7 in March, the strongest factory reading since August 2022.

March payrolls added 178,000 jobs.

Prime-age labor force participation sits near multi-decade highs.

Those numbers are real.

Every one of them.

Late cycles always look strongest at the top.

The surface holds while the foundation cracks.

The headline data stays elevated while the structural deterioration builds underneath.

Then the gap closes, violently, all at once.

And everyone pointing at the headline data acts surprised.

The Documents Always Win

Michael Burry read the mortgage documents in 2006 when everyone else was reading the press releases.

The documents said something completely different.

The market spent another year proving the press releases right.

Before the documents won.

The documents always win eventually.

That is the only thing the history of markets teaches with any consistency.

The Consumer’s Verdict

The University of Michigan consumer sentiment index hit 47.6 in April 2026.

The worst reading in the survey’s 74-year history.

The previous record was 50.0, set in June 2022 when inflation was running at 9 percent.

One-year inflation expectations now sit at 4.8 percent, up from 3.8 percent in March.

The consumer has not gotten nervous.

The consumer has reached a conclusion and is sitting with it.

The Data Beneath the Surface

The BLS revised February payrolls to –133,000, worse than the initial –92,000 print.

Fourth-quarter 2025 GDP came in at 0.5 percent annualized, revised down from 1.4 percent.

EY-Parthenon’s chief economist called 2025 “the year that could have been.”

His description of 2026 was less diplomatic.

The Middle East conflict makes the outlook even worse.

Translated into plain language:

A war-driven stagflation environment with no clean policy response available.

The Policy Trap

March CPI came in at +3.3 percent year over year, up sharply from 2.4 percent in February.

Energy up 10.9 percent.

Gasoline up 21.2 percent.

The Iran war is already showing up in the monthly inflation data the Fed must manage.

Jerome Powell has already warned publicly of a new energy supply shock and said no one knows how large it will be.

The Fed chair is acknowledging on the record that the central variable in his policy decision is outside his control.

In The Math Behind the Final Stretch published January 2026 the trap was laid out precisely:

Cut rates and inflation accelerates.

Hold rates and the labor market fractures further.

There is no third option.

The administration that built this trap also purged the officials whose institutional job was to stop it from forming.

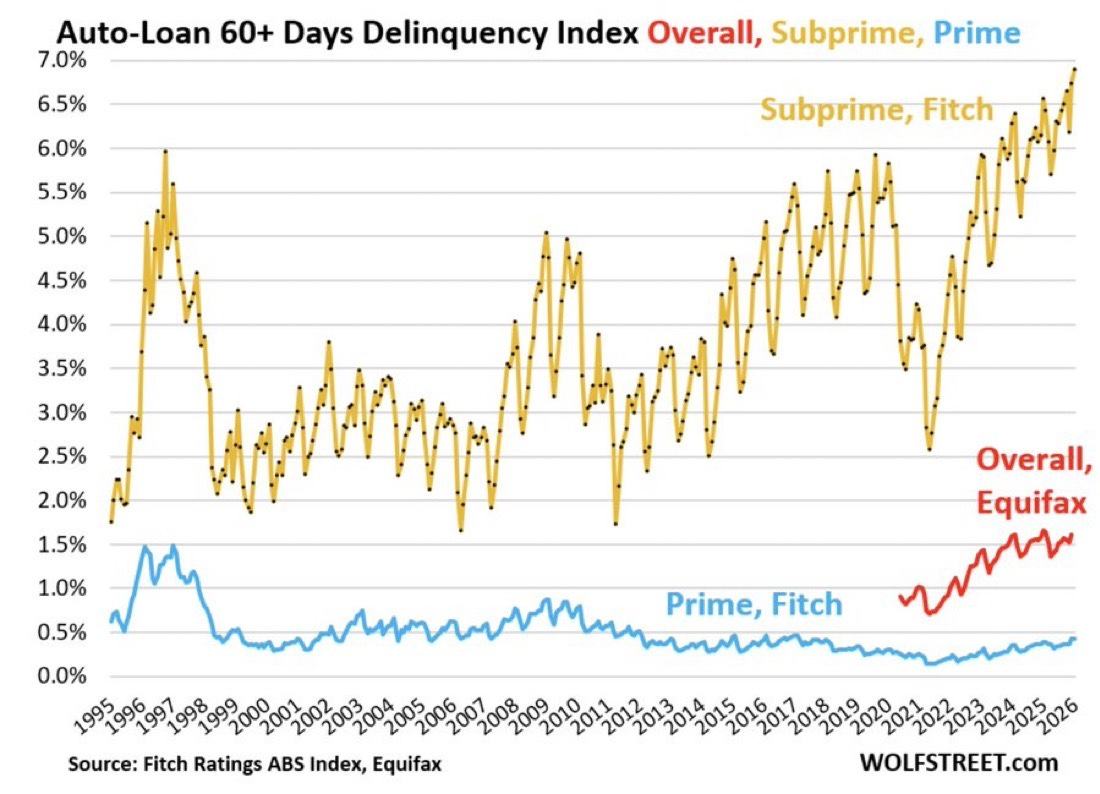

The Household Stress Test

Total US household debt now stands at $18.8 trillion.

Auto-loan 90-day delinquency rates have reached 5.2 percent, essentially tied with the GFC peak of 5.3 percent in 2010.

A 15-year high.

Student-loan flow into serious delinquency now sits at 16.2 percent, a 21-year record.

Roughly nine million borrowers are now in default.

The largest number ever recorded.

In November 2025 in Why American Families Are Breaking Before the Economy Does I wrote that consumer delinquencies precede official recession by six to eighteen months in every cycle without exception.

Families always feel cycles first.

That piece was published five months ago.

The data has not stabilized.

It has deteriorated across every series I track.

The Two Economies

Rasmussen’s April 2026 survey finds 44 percent of Americans say their personal finances have worsened in the past six months, up from 36 percent in October 2025.

Only 10 percent say things are going well nationally.

Harvard-Harris March 2026 finds 53 percent say the economy is worse under Trump than under Biden.

The market and the household are looking at the same economy.

And reaching completely different conclusions.

That gap is the late-cycle signal.

It always closes.

The only open question is which direction.

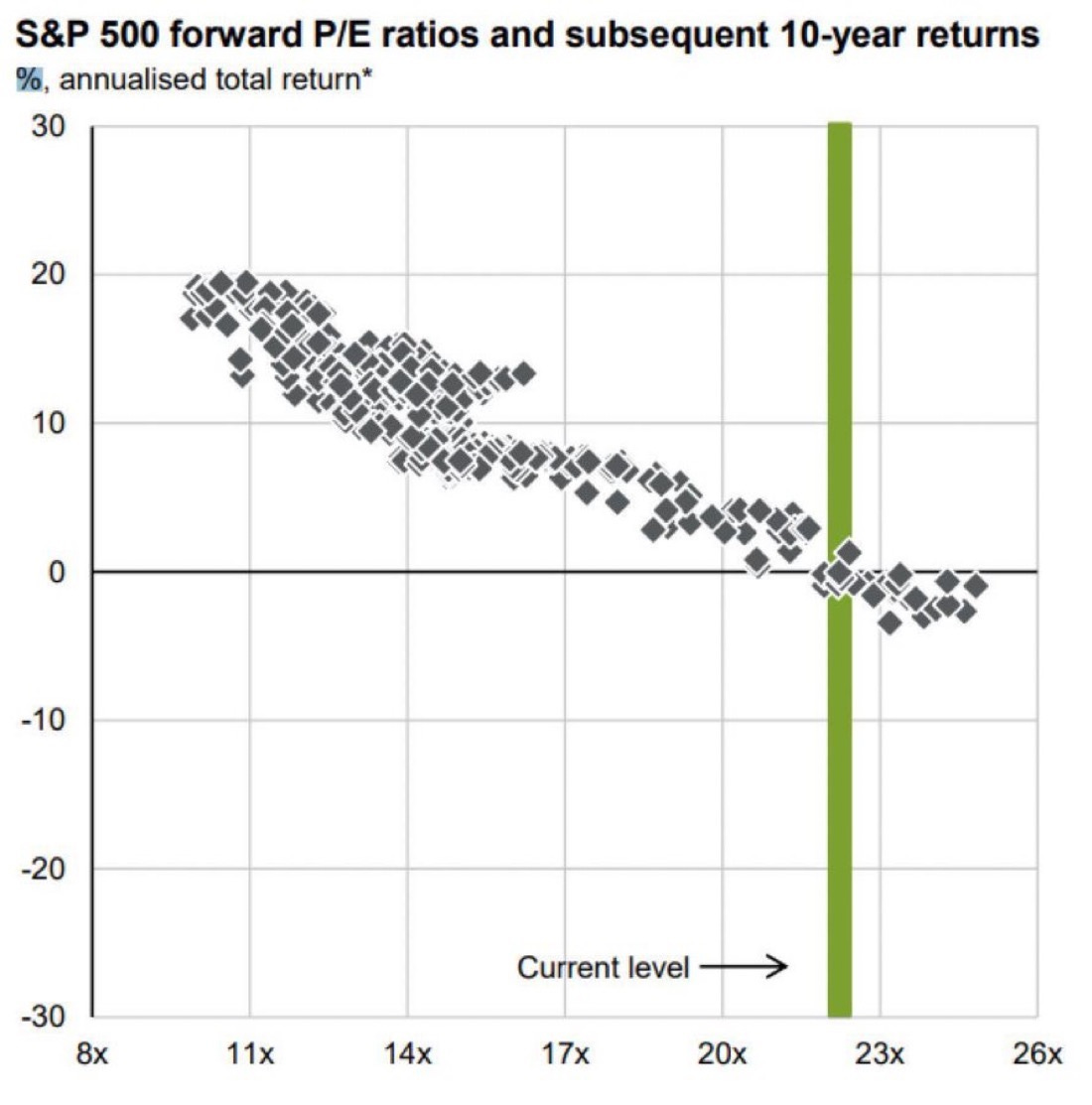

Terminal Valuations

Valuation extremes are the fuel.

The numbers are not subtle:

Trailing S&P 500 P/E: 30.55

Shiller CAPE ratio: 40.36

Nvidia P/E: 41.3

Wilshire 5000 to GDP: 226.7 percent

Those are terminal-cycle readings.

The trigger is oil.

When crude breaks back above 105 to 110 and begins transmitting into monthly inflation gauges in a sustained way, the Fed’s already limited options narrow to essentially zero.

The closed strait makes that scenario structurally likely.

The setup has been in place for months.

Short-Term Market Read

7,050 is the level that matters this week.

Hold it and it may function as weekly support.

Lose it and watch whether it converts to resistance, opening a path toward 6,950.

A weekly close below 6,900 after failing to hold recent levels would represent a textbook rejection of new all-time highs and a strong structural bearish signal.

Weeks of balance near the top without a decisive breakout higher are slower but equally bearish.

With a tight stop near 7,200.

The Arithmetic of the Cycle

Modeled downside range: 2,500 to 3,250.

Sequence:

Valuation compression → earnings revision → credit stress.

A false-hope rally in early 2027 will trap late-cycle capital the same way every false-hope rally in every prior cycle has trapped late-cycle capital.

The true bottom forms late 2027 through early 2028.

Every falsification condition published in January 2026 remains unmet.

Buffett says the market can stay irrational longer than you can stay solvent.

True.

Also incomplete.

Markets can delay arithmetic.

They have never once avoided it.

Positioning

Long VIX.

Long oil.

Short SPX.

All established before the conflict.

All disclosed.

All still open.

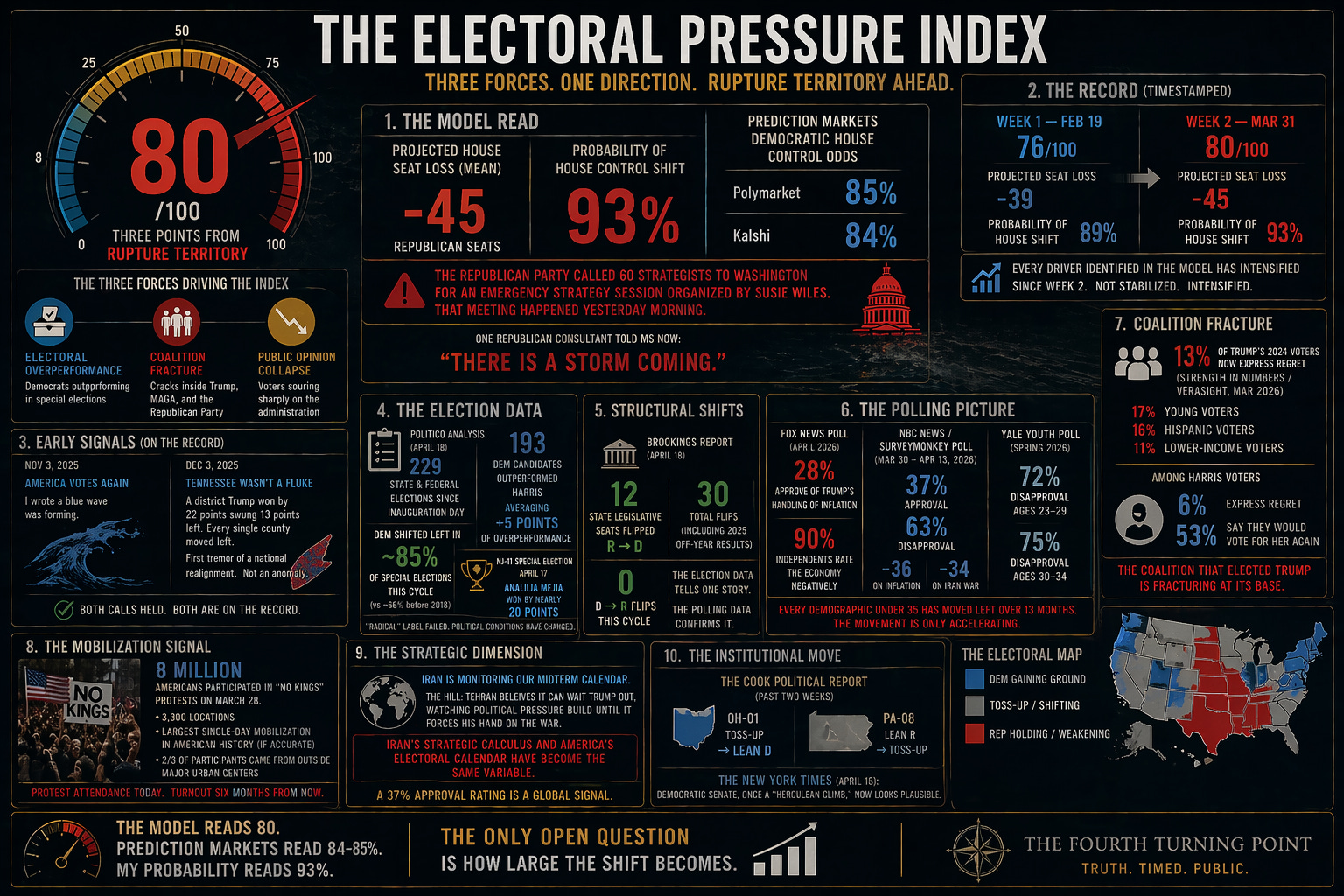

The Electoral Pressure Index

Three forces now drive the Electoral Pressure Index toward rupture territory: electoral overperformance in special elections, coalition fracture inside Donald Trump, MAGA, and the Republican Party, and public opinion shifting sharply against the administration.

The EPI reads 80 on a 0–100 scale.

Three points from Rupture Territory.

My model projects a mean Republican seat loss of 45 House seats with a 93 percent probability of a House control shift.

Prediction markets see the same direction.

Polymarket prices Democratic House control at 85 percent.

Kalshi prices it at 84 percent.

Institutional forecasters are beginning to move as well.

The Cook Political Report shifted OH-01 from toss-up to lean Democratic and PA-08 from lean Republican to toss-up in the past two weeks.

The New York Times reported yesterday that a Democratic Senate, described as recently as last August as a herculean climb, now looks plausible.

One Republican consultant told MS NOW yesterday:

“There is a storm coming.”

The Trump campaign called 60 Republican strategists to Washington for an emergency strategy session organized by Susie Wiles.

That meeting happened yesterday morning.

The Record

The record is timestamped.

EPI Week 1, published February 19, placed the index at 76, projecting a 39-seat Republican loss with an 89 percent probability of a House control shift.

Week 2, published March 31, moved the index to 80, widening the mean projection to −45 seats and raising the probability of a House control shift to 93 percent as every structural driver deteriorated simultaneously.

Every driver identified in the original model has since intensified.

Not stabilized.

Intensified across the board.

Early Signals

In America Votes Again, published November 3, 2025, I wrote that a blue wave was forming.

In Tennessee Wasn’t a Fluke, published December 3, 2025, I wrote that a district Trump won by 22 points swinging 13 points left, with every single county moving in the same direction, was the first tremor of a national realignment.

Not an anomaly.

Both calls held.

Both are on the record.

The Election Data

A Politico analysis published April 18 examined 229 state and federal elections since inauguration day.

Democratic candidates outperformed Harris in 193 of them, averaging five points of overperformance.

In the cycle heading into 2018, Democrats shifted races left in about two-thirds of special elections.

That cycle produced a 40-seat Democratic wave.

This cycle Democrats have shifted races left in close to 85 percent of elections.

Last Thursday Analilia Mejia, a former Bernie Sanders campaign staffer, won New Jersey’s 11th Congressional District by nearly 20 points.

Republicans had designated the district as proof that the “radical” label could work.

She won by 20 points.

The label failed because the political conditions that once made it effective no longer exist.

Structural Shifts

A Brookings report published April 16 found:

• 12 state legislative seats flipped Republican to Democratic this cycle

• 30 flips total counting 2025 off-year results

Flips in the opposite direction:

Zero.

The election data tells one story.

The polling data now confirms it.

The Polling Picture

The polling picture is moving in one direction.

Fox News polling shows:

• 28 percent approval of Trump’s handling of inflation

• 90 percent of independents rating the economy negatively

The NBC News / SurveyMonkey poll, conducted March 30 through April 13, shows:

• 37 percent approval

• 63 percent disapproval

Issue breakdown:

• –36 on inflation

• –34 on the Iran war

The Yale Youth Poll (Spring 2026) shows:

• 72 percent disapproval among voters aged 23–29

• 75 percent disapproval among voters aged 30–34

Every demographic bucket under 35 has moved in the same direction across 13 months.

The movement is only accelerating.

Coalition Fracture

Thirteen percent of Trump’s 2024 voters now express regret, according to Strength in Numbers / Verasight (March 2026).

The regret concentrates among the voters who formed the core of Trump’s winning coalition:

• 17 percent among young voters

• 16 percent among Hispanic voters

• 11 percent among lower-income voters

Those are the exact groups that gave Trump his 2024 margin.

Among Harris voters:

• only 6 percent express regret

• 53 percent say they would vote for her again

The coalition that elected Trump is fracturing at its base.

The coalition that opposed him is not.

The Mobilization Signal

On March 28, organizers estimated 8 million Americans participated in “No Kings” protests across 3,300 locations.

If accurate, that would represent the largest single-day mobilization in American history.

More than two-thirds of participants came from outside major urban centers.

Places like:

• Lebanon, Pennsylvania

• Midland, Texas

• Boise, Idaho

People did not drive to those events for a Tuesday morning news cycle.

They drove because something shifted in how they understand what is happening to their country.

That shift shows up first in protest attendance.

It shows up six months later in turnout.

The Strategic Dimension

There is a dimension to this that most electoral analysis misses.

The Iranian government is actively monitoring the American midterm calendar.

Analysts cited in The Hill yesterday say Tehran believes it can wait Trump out, watching political pressure build until it forces his hand on the war.

Iran’s strategic calculus and America’s electoral calendar have become the same variable.

A foreign government is making military and diplomatic decisions partly based on its read of American midterm dynamics.

That is what a 37 percent approval rating represents on the world stage.

The Model

The model reads 80.

Prediction markets read 84–85 percent.

My probability reads 93 percent.

The Republican Party called an emergency strategy session in Washington yesterday.

The trend across the datasets is the same.

The only open question now is how large the shift becomes.

What Comes Next

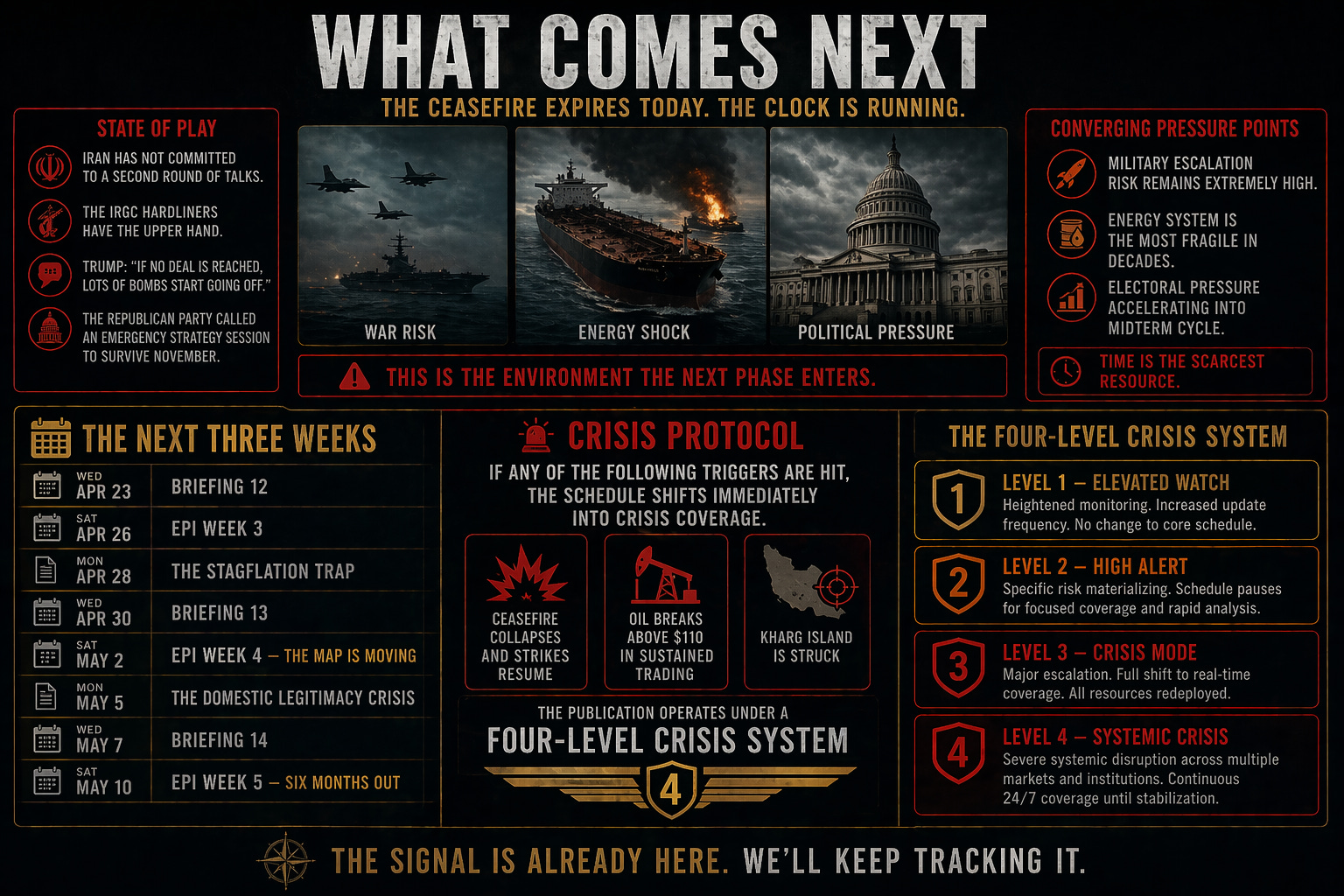

The ceasefire expires today. Iran has not committed to the second round of talks. The IRGC hardliners have the upper hand.

Trump said that if no deal is reached, “lots of bombs start going off.”

At the same time, the Republican Party has called an emergency strategy session to determine how it survives November.

This is the environment the next phase of this publication enters.

The Next Three Weeks

The work continues on the following schedule:

Wednesday, April 23

Briefing 12

Saturday, April 26

EPI Week 3

Monday, April 28

The Stagflation Trap

Wednesday, April 30

Briefing 13

Saturday, May 2

EPI Week 4 — The map is moving

Monday, May 5

The Domestic Legitimacy Crisis

Wednesday, May 7

Briefing 14

Saturday, May 10

EPI Week 5 — Six Months Out

Crisis Protocol

If the ceasefire collapses and strikes resume, if oil breaks above $110 in sustained trading, or if Kharg Island is struck, the schedule shifts immediately into crisis coverage.

The publication operates under a four-level crisis system.

It has never been more relevant.

If events require it, it will be used.

A Note at the End

I started this publication on July 29, 2025 with two subscribers and a thesis most people were not ready to hear.

Markets, politics, and institutions move together.

The most consequential moments in history occur when all three begin breaking at the same time.

Finding the signal before it becomes the headline is not just possible.

It is necessary.

Two hundred and sixty-five days later, that thesis has become the operating environment.

I am twenty-two years old. I built this from a gap year with no institutional backing, no political machine, and no one telling me what conclusions to reach.

The only thing this publication has ever run on is the work itself and the belief that the work matters.

The Institution

I want this to become something that lasts.

Not just a newsletter people open on a Tuesday afternoon, but a genuine analytical institution with a public record that speaks for itself over years.

I want to walk into rooms that once would not have had me and be taken seriously because the analysis earned it.

I want to be part of the generation that steps forward when the institutions that were supposed to hold begin to fail.

I believe that generation exists.

I believe they are reading this.

The Principles

Beyond the publication, I want a life built on the same principles the writing reflects.

Depth over speed.

Honesty over comfort.

The willingness to be early and visible and wrong in public rather than safe and silent and irrelevant.

I want to build something in markets, in politics, and in civic life that reflects what I actually believe about how the world works and what it requires from the people who can see what is coming.

The Foundation

The work is the foundation.

Everything else gets built on top of it.

This is the moment The Fourth Turning Point was built for.

The work continues.

The record stays public.

The positions stay disclosed.

Systems rarely break in isolation.

Markets, politics, and institutions move together.

And the moments when they begin breaking at the same time are the moments that shape history.

That is what The Fourth Turning Point exists to study while it is still happening.

Amazing work! Reminds me a lot of what Charlie Garcia is saying as well.

Your highly detailed explanation of the coinciding events which changed our history is amazing!!!